![Discover the Top 10 FinTech Trends & Innovations [2025-2026]](https://www.startus-insights.com/wp-content/uploads/2025/06/FinTech-Trends-SharedImg-StartUs-Insights-noresize-420x236.webp)

Accelerate Productivity in 2025

Reignite Growth Despite the Global Slowdown

Executive Summary: What are the Top 10 FinTech Trends in 2025 & Beyond?

Valued at USD 394.88 billion in 2025, the market is projected to grow to USD 1126.64 billion by 2032, reflecting a CAGR of 16.2%. Beyond scale, the industry is evolving in scope, integrating fintech trends such as AI, decentralization, sustainability, and embedded solutions into core operations. The top fintech trends shaping the sector are:

- Green and Sustainable Finance – ESG-driven regulations and investor pressure are fueling sustainable lending, green bonds, and carbon analytics. Blockchain ensures traceability, while AI powers ESG scoring, helping reallocate capital toward climate-positive outcomes.

- Cybersecurity Innovations – As attack surfaces expand through APIs, open banking, and real-time payments, fintechs are deploying AI threat detection, behavioral biometrics, and quantum-resistant encryption to safeguard trust and comply with evolving regulations.

- Decentralized Finance (DeFi) – With USD 60 billion+ locked in DeFi protocols, decentralized lending, tokenized assets, and smart contract automation are empowering financial access in underserved regions and reshaping how institutions approach yield, custody, and cross-border payments.

- Generative AI Integration – AI copilots, NLP-powered assistants, and LLM-trained compliance tools are optimizing customer service, fraud prevention, onboarding, and wealth advisory, driving a projected USD 16.4 billion GenAI-in-Fintech market by 2032.

- Expansion of Inclusive Finance – UPI, Pix, and BaaS platforms are expanding financial inclusion via mobile-first services, alternative credit scoring, and microloans. Fintechs use AI and IoT to serve gig workers, smallholders, and migrants across the Global South.

- WealthTech – Robo-advisors, tokenized funds, and consolidated financial dashboards are democratizing investment access. AI copilots and blockchain-backed audit trails improve client insights, compliance, and personalization at scale.

- Open Banking – Over 1.5 billion API calls per week in Brazil and 13% consumer adoption in the UK signal global momentum. Aggregators, account information services, and behavioral biometrics support secure data sharing and instant financial experiences.

- Regulatory Technology (RegTech) – With AML, DORA, and eKYC compliance intensifying, fintechs are deploying AI, NLP, and RPA to reduce false positives, automate audits, and streamline global reporting across highly regulated jurisdictions.

- Embedded Finance – USD 1.73 trillion by 2034; embedded payments, lending, and insurance are reshaping digital commerce. Low-code APIs and BaaS platforms allow non-financial firms to deliver seamless financial products directly within apps.

- Central Bank Digital Currency (CBDC) – With 134+ countries piloting CBDCs, programmable sovereign currencies are enabling smart disbursements, real-time settlements, and offline payments, transforming monetary policy execution and financial inclusion.

Read on to explore each trend in depth – uncover key drivers, current market stats, cutting-edge innovations, and 20 leading startups shaping the future of financial technology.

Frequently Asked Questions

1. How is FinTech shaping the future of banking?

FinTech is transforming banking into a real-time, API-enabled ecosystem – driven by open banking, AI, embedded finance, and digital onboarding—that offers hyper-personalized, on-demand financial services.

2. Is FinTech the future of finance?

Yes, fintech is redefining global finance by enabling decentralized systems, digital currencies, and inclusive financial access, with the industry expected to reach USD 1126.64 billion by 2032.

3. What is the future of FinTech?

The future of fintech lies in autonomous finance, generative AI, tokenization, and programmable money like CBDCs, all converging to build secure, transparent, and borderless financial infrastructure.

4. How is FinTech changing financial services?

FinTech is streamlining financial services through AI-driven automation, real-time data insights, digital identity, and mobile-first platforms – lowering costs, improving reach, and enhancing user experience at scale.

Methodology: How We Created the FinTech Trend Report

For our trend reports, we leverage our proprietary StartUs Insights Discovery Platform, covering 7M+ global startups, 20K technologies & trends plus 150M+ patents, news articles, and market reports.

Creating a report involves approximately 40 hours of analysis. We evaluate our own startup data and complement these insights with external research, including industry reports, news articles, and market analyses. This process enables us to identify the most impactful and innovative trends in the finance industry.

For each trend, we select two exemplary startups that meet the following criteria:

- Relevance: Their product, technology, or solution aligns with the trend.

- Founding Year: Established between 2020 and 2025.

- Company Size: A maximum of 200 employees.

- Location: Specific geographic considerations.

This approach ensures our reports provide reliable, actionable insights into the fintech innovation ecosystem while highlighting startups driving technological advancements in the industry.

Innovation Map outlines the Top 10 Trends in the FinTech Industry & 20 Promising Startups

For this in-depth research on the Top FinTech Trends & Startups, we analyzed a sample of 5100+ global startups & scaleups. The FinTech Innovation Map created from this data-driven research helps you improve strategic decision-making by giving you a comprehensive overview of the finance industry trends & startups that impact your company.

Tree Map reveals the Impact of the Top 10 Financial Technology Trends

FinTech is rapidly emerging in 2025, driven by trends such as green finance and decentralized models, reshaping access, transparency, and sustainability in financial services. Generative AI (Gen AI) and cybersecurity innovations improve fraud detection, risk modeling, and compliance at scale.

Meanwhile, inclusive finance, open banking, and embedded finance unlock hyper-personalized, smooth access to credit, savings, and payments. WealthTech and RegTech platforms increase advisory efficiency and regulatory alignment, while central bank digital currencies (CBDCs) modernize sovereign payment systems.

These innovations reflect the financial technology sector’s push toward real-time, democratized, and secure financial infrastructure.

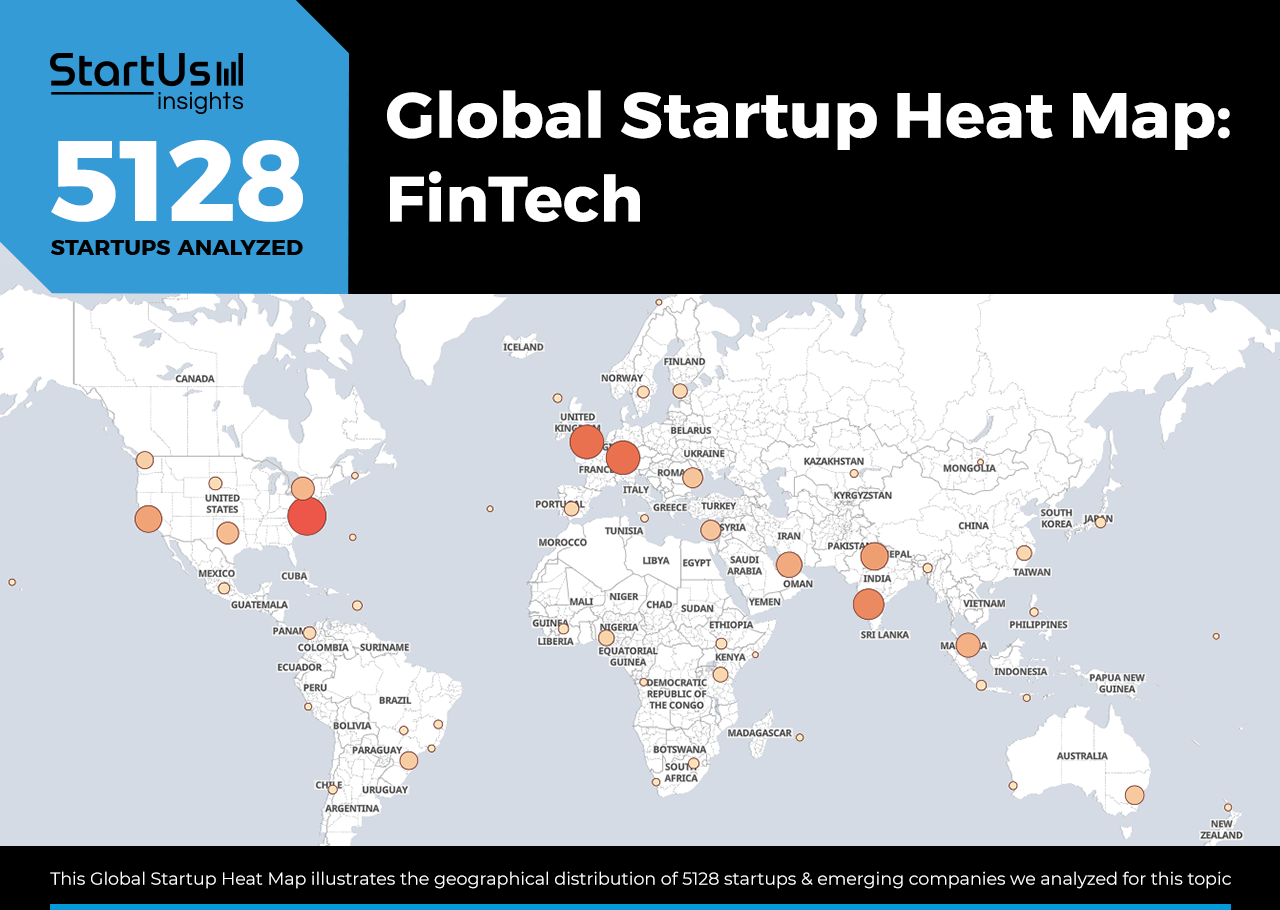

Global Startup Heat Map covers 5100+ FinTech Startups & Scaleups

The Global Startup Heat Map showcases the distribution of 5100+ exemplary startups and scaleups analyzed using the StartUs Insights Discovery Platform. It highlights high startup activity in the United States and Western Europe, followed by India. From these, 20 promising startups are featured below, selected based on factors like founding year, location, and funding.

Want to Explore FinTech Innovations & Trends?

Top 10 Technology Trends in the Finance Industry [2025 and Beyond]

1. Green and Sustainable Finance: Market to Grow at a CAGR of 22.4%

Regulatory mandates, rising environmental, social, and governance (ESG) priorities, and increasing investor demand drive green and sustainable finance. For example, the European Union’s (EU) Green Deal requires financial institutions to direct capital toward sustainable activities.

And taxonomy regulation plays a vital role in enabling the EU to scale up sustainable investment. Further, the Sustainable Finance Disclosure Regulation (SFDR) requires financial institutions to assess how sustainability risks are integrated into the investment decision process.

Credit: Global Market Estimates

In response, the global green fintech market is projected to grow at a CAGR of 22.4% till 2029. This positions green fintech as a high-impact driver of the future financial ecosystem.

Additionally, digital lending platforms offer preferential loans for clean energy, electric vehicles (EVs), and sustainable agriculture, powered by artificial intelligence (AI)-based underwriting.

Similarly, blockchain platforms facilitate the transparent issuance of green bonds and tokenized carbon credits. This reduces compliance costs, improves capital allocation, and ensures accountability. Stripe Climate, for example, lets businesses track and offset emissions through financial transactions.

AI and machine learning (ML) power ESG scoring models for green credit assessment. These technologies allow lenders to assess climate-related credit risks and fund low-carbon projects with better accuracy.

Big data analytics platforms integrate environmental, financial, and operational data to calculate carbon footprints. These platforms also allow users to monitor sustainability key performance indicators (KPIs) and generate actionable insights for green investment strategies. For example, Arabesque S-Ray offers ESG data analytics by combining big data and machine learning to generate sustainability scores and insights.

Another instance is that of Clarity AI, which uses AI, ML, and big data analytics to offer ESG scoring, portfolio screening, and carbon-footprint measurement tools.

Likewise, blockchain and distributed ledger technology (DLT) ensure traceability and integrity in green financing. These solutions validate green bond proceeds and certify carbon credit transactions. Allinfra Climate, for instance, verifies that funds raised through green bonds are spent on legitimate sustainable projects and certifies carbon credit transactions to prevent double-counting.

Further, internet of things (IoT) devices collect real-time environmental data from assets like smart meters or electric fleets. This data feeds into sustainability-linked financial products to enable dynamic pricing and support usage-based lending or insurance models.

Zend delivers Sustainability as a Service (SaaS) Platform for ESG Financial Reporting

UK-based startup Zend offers a decentralized fintech platform that converts everyday financial transactions into a measurable environmental impact.

The platform integrates an AI-powered validation engine into banking systems. This enables businesses to calculate, verify, and monetize their carbon footprint in real time.

Credit: Zend

Moreover, using its proprietary Impact Chain, which is a blockchain-based validation protocol, the startup employs a proof-of-impact mechanism to ensure transparent and accurate climate data.

Additionally, its accounts support multi-currency payments, money exchange at preferred rates, and access to thousands of partner deals. The startup also allows businesses to earn dividends by monetizing their oxygen assets.

For families, Zend uses Zave savings, the Zend money marketplace, and its AI-powered carbon calculator to simplify carbon offsetting and sustainable finance for individuals and businesses.

Its enterprise suite further supports cross-border payments, environmental, social, and governance (ESG) tracking, and compliance screening via the Valid8 engine.

Digiup provides a Sustainable Trade Grading Platform

Indian startup Digiup creates an AI-enabled digital platform that integrates sustainability into trade operations to increase green and sustainable finance.

The platform embeds ESG assessment tools directly into supply chain finance workflows. This allows financial institutions and corporations to measure, implement, and monitor sustainability performance in real-time.

Moreover, using ESG due diligence engines and contextualized AI components, the platform automates compliance checks and supports sustainability-linked finance decisions.

In addition, Digiup offers IoT modules and adapters to increase data traceability and connect systems through green finance portal plugins that streamline reporting.

Through its sustainable finance analytics layer, the startup further ensures full transparency across transactions.

2. Cybersecurity Innovations: AI-led Analytics Spots Fraud & Prevents Breaches

Cybersecurity innovations are essential to the fintech industry as digital platforms face complex threats, regulatory pressures, and the need to protect user trust.

The expansion of mobile wallets, open banking application programming interfaces (APIs), and instant payments is widening the attack surface. These innovations are attracting cyberattacks, including ransomware-as-a-service and phishing schemes.

In parallel, stricter data privacy mandates are pushing fintech companies to adopt proactive security measures to ensure compliance and safeguard sensitive data. For example, the EU’s General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) drive fintech firms to adopt stronger security measures to comply and protect customer data.

Real-time fraud detection, encryption, and AI-driven risk analytics also prevent data breaches, reduce fraud-related losses, and automate regulatory compliance. For example, Mastercard’s Decision Intelligence and Visa Advanced Authorization use AI-powered analytics to spot fraud, prevent breaches, and streamline compliance.

More importantly, strong security practices build customer confidence and position fintechs as reliable partners. For instance, behavioral monitoring, secure-by-design development practices, and AI-based anomaly detection increase reputational and regulatory resilience.

Moreover, identity and access management (IAM) systems use multi-factor authentication (MFA) and behavioral biometrics to secure access points. Okta and Auth0, for instance, use MFA and behavioral biometrics like keystroke and mouse patterns to secure fintech access. Zero trust architecture (ZTA) also enforces continuous verification and least privilege access.

Fintechs invest in securing APIs and third-party integrations using DevSecOps, transport layer security (TLS), and API gateways to prevent data leakage and denial-of-service attacks.

Quantum-resistant encryption, for example, lattice-based algorithms, which involve complex mathematical structures, is piloted to prepare for future quantum threats. Biometric authentication, including fingerprint, facial, and voice recognition, is replacing passwords in mobile fintech apps.

Also, cloud-native application protection platforms (CNAPPs) and micro-segmentation safeguard dynamic architectures. These solutions are especially relevant to fintechs running containerized and serverless environments that require constant protection.

Meanwhile, blockchain technology enhances auditability and data integrity, particularly in identity verification and transaction logging. ConsenSys and IBM Blockchain are two instances that support identity checks, secure logs, and tamper-proof financial processes.

Further, the cybersecurity-in-fintech market is projected to grow to approximately USD 46 billion by 2032, at a CAGR of 9.95%.

Cyble offers AI-powered Threat Intelligence Platforms

US-based startup Cyble provides AI-native cybersecurity platforms that protect financial institutions against evolving digital threats. These platforms combine proprietary AI technologies with deep-threat intelligence capabilities.

Notably, its products include Cyble Vision for attack surface management, Cyble Hawk for proactive threat detection, and ODIN for internet asset scanning. These solutions continuously monitor the dark web, analyze threat actor behavior, and detect vulnerabilities. They also enable fintech organizations to mitigate risks before incidents occur.

Moreover, Cyble integrates solutions such as predictive threat intelligence, vulnerability management, brand intelligence, and executive monitoring. This integration allows financial firms to navigate complex regulatory requirements while safeguarding customer trust.

Nefture monitors Real-time DeFi Security and Risk Analytics

French startup Nefture delivers a real-time decentralized finance (DeFi) security and risk analytics platform that safeguards digital assets and monitors on-chain threats.

The platform connects instantly to any wallet without setup or signature and begins tracking portfolio performance, risk exposure, and yield metrics across DeFi positions.

Moreover, the platform uses customizable threat detection with severity thresholds to identify liquidations, depegs, and exploits. The platform also simultaneously flags arbitrage opportunities and annual percentage yield (APY) shifts.

It combines cross-chain aggregation with institutional-grade security to offer a unified dashboard for trade execution, alerts, and analytics.

Nefture further enables businesses to actively manage DeFi exposure and mitigate risk in real time by integrating security and performance monitoring in one system.

3. Decentralized Finance (DeFi): Market to Reach USD 1558 B by 2034

DeFi is innovating the global fintech landscape through growing cryptocurrency adoption, rising demand for decentralized alternatives, and increasing financial inclusion.

As digital assets gain popularity in both developed and emerging markets, the need for on-chain financial services is increasing. In regions like Latin America and Sub-Saharan Africa, where banking access is limited and currency instability is common, DeFi adoption is particularly strong. It offers businesses permissionless access to savings, lending, and payments.

DeFi is improving the fintech sector by creating new financial models that bypass traditional institutions and enable open, programmable systems. Its growth signals a shift toward decentralized, transparent, and globally accessible financial services. DeFi also extends beyond cryptocurrencies into tokenized assets, decentralized exchanges, and digital identity. Fintech firms are integrating DeFi to launch innovative products, reduce costs, and serve underserved markets. For example, Revolut offers crypto staking services, and PayPal supports stablecoin payments to facilitate faster cross-border transactions.

Moreover, decentralized lending platform Aave allows businesses to earn yield or access loans without banks. Asset tokenization is also rising, with Franklin Templeton’s tokenized US Government Money Market Fund surpassing USD 760 million in assets. DeFi also streamlines cross-border payments using stablecoins and smart contracts, as seen in Visa and PayPal’s adoption of stablecoin-based settlements.

Smart contracts automate value transfers and enforce rules without intermediaries. Cross-chain interoperability connects blockchain ecosystems and expands asset access. Likewise, layer 2 solutions, for example, zero-knowledge rollups, require high transaction throughput and low fees to support real-time lending, trading, and payments at scale.

Additionally, cryptographic innovations, including zero-knowledge, allow data verification without revealing sensitive details. And quantum-resistant encryption protects data against future quantum attacks. This increases privacy and resilience in the fintech sector.

Credit: Precedence Research

Further, the global DeFi market is projected to reach USD 1558.15 billion by 2034, growing at a CAGR of 53.8% from 2025.

Institutional and venture investments are also rising, which reflects growing confidence in the DeFi ecosystem. As of mid-June 2025, total value locked (TVL) in DeFi lending protocols stood at around USD 60 billion. While crypto-native asset managers controlled over USD 4 billion in on-chain capital.

Definitive Finance offers an Institutional-grade DeFi Trading Platform

US-based startup Definitive Finance creates a decentralized trading platform that enables businesses to trade any asset across any blockchain using advanced order types.

The platform aggregates liquidity and pricing data from multiple chains that allow businesses to access deeper markets and execute trades at optimal prices through a single interface.

The startup also offers its proprietary utility token, $EDGE, which businesses stake to reduce fees, gain priority access to new features, and earn tailored rewards.

Additionally, $EDGE powers the platform’s user incentives, with token airdrops targeting the most active on-chain traders.

As a result, Definitive Finance streamlines cross-chain trading, unifies fragmented liquidity, and delivers an integrated DeFi experience for high-frequency and professional traders.

Fintopio combines a Dual-mode CeFi and DeFi Wallet

UAE-based startup Fintopio provides a dual-mode digital wallet that combines centralized finance (CeFi) and DeFi in a single platform. It enables businesses to switch instantly between custodial transactions and full asset control.

The platform also supports over 100 assets across more than 30 blockchains with on-chain and cross-chain swap functionality.

Additionally, it offers easy access through the web, iOS, Android, and Telegram MiniApp. This offers a consistent experience across devices.

Credit: Fintopio

The startup integrates Smart Send, which allows businesses to transfer crypto by social media usernames directly within Telegram or X, while it also supports crypto gifting to recipients without wallets.

Further, Fintopio includes full non-fungible token (NFT) and decentralized application (dApp) support across Ethereum, Polygon, Solana, and TON.

4. Generative AI Integration: 43% of Finance Professionals Already using GenAI Solutions

GenAI is driven by growing demand for hyper-personalized financial services, rising regulatory scrutiny, and competitive pressure from digital-first challengers.

As customers expect real-time experiences and regulators urge firms to stress-test AI models, financial institutions are turning to GenAI to optimize operations and improve service delivery.

Moreover, the market for GenAI in fintech is projected to surge to USD 16.4 billion by 2032. It is growing at a CAGR of 31% till 2033. Another study forecasts near-term revenue growth of up to USD 2.17 billion in 2025, marking an even sharper 35.3% CAGR. Thus, the GenAI adoption is scaling quickly, with 43% of finance professionals already using GenAI tools, while 55% are actively evaluating them.

In addition, language-model-powered fraud detection tools reduce false positives by over 60% and detect anomalies within milliseconds. This improves both regulatory compliance and customer protection across fintech platforms. Financial advisors also gain instant insights from GenAI-generated summaries of filings and market chatter.

Fintech platforms use natural language processing (NLP) to interpret financial documents, chats, and disclosures, transforming unstructured data into actionable insights. For example, Morgan Stanley’s AI assistant addresses the needs of the bank’s investment banking, sales and trading, and research staff.

Similarly, fintech companies use robotic process automation (RPA) alongside GenAI to automate workflows such as KYC, compliance checks, and onboarding, enabling faster and more scalable operations. GenAI to automate workflows such as KYC, compliance checks, and onboarding. This enables faster and more scalable fintech operations.

Transformer-based deep learning models drive contextual decision-making across lending, investments, and customer service. These deep learning models underpin Klarna’s AI assistant, which resolves two-thirds of all customer support chats.

Also, low-code orchestration platforms enable fintech firms to rapidly deploy GenAI tools across apps. For example, Nubank uses GPT-4o vision through an orchestration setup, which is their internal AI ecosystem, to analyze visual and textual data for fraud detection.

Further, elastic cloud graphics processing units (GPUs) support large-scale real-time processing for fintech operations such as transaction monitoring, customer service automation, and fraud analytics.

Rogo AI provides Custom-trained Financial LLMs

US-based startup Rogo AI deploys a generative AI platform that automates financial workflows and unifies firm-specific data in a secure system.

The platform custom-trains large language models (LLMs) using professionally labeled financial data to generate reports, streamline analysis, and support decision-making.

Moreover, it combines an interactive AI table interface for real-time data sorting and filtering with automated material creation tools that change raw inputs into structured summaries and presentations.

Additionally, the platform integrates prompt libraries for workflow automation, enables proprietary document interrogation, and connects with internal and external data sources.

Rogo AI further enforces enterprise-level security through single-tenant deployment, granular permissions, and compliance with SOC 2, CCPA standards, and more.

Unique deploys Agentic AI Agents for Finance Workflows

Swiss-based startup Unique develops a generative AI platform that equips financial institutions with secure, customizable AI agents.

The AI agents automate tasks, improve client engagement, and enhance data accuracy. It also processes internal documents and client interactions to generate investment research summaries and personalized recommendations. They also structure overviews for know-your-customer (KYC) compliance.

Moreover, the platform streamlines response generation for requests for information (RFIs) using past documents and organizational data.

Credit: Unique

Additionally, Unique enables admins and data scientists to build tailored AI spaces, configure assistant behavior, and control access based on team roles. It also integrates with existing knowledge sources like SharePoint and Confluence.

The startup also supports the ingestion of unlimited documents across formats and scales without compromising performance.

To maintain compliance, the startup further embeds feedback mechanisms, automated quality checks, and role-based governance features.

5. Expansion of Inclusive Finance: Enabling Banking Services in Remote Areas

The expansion of inclusive finance is driven by rapid mobile adoption, low-cost internet, and policy-led digital infrastructure. Instant payment systems, for example, India’s unified payments interface (UPI) and Brazil’s Pix, are lowering barriers to formal financial access.

In parallel, governments are advancing digital public infrastructure and proportionate e-money regulation that enable fintechs to reach the unbanked population.

Credit: Precedence Research

Fintechs are also expanding access to credit. Digital lending platforms are key to expanding financial access for underserved borrowers. This digital lending platform market is forecasted to grow to USD 13.8 billion by 2025 and is anticipated to reach around USD 114.72 billion by 2034, representing a 26.53% CAGR.

Credit: Research and Markets

Moreover, global peer-to-peer (P2P) lending is projected to reach USD 251.3 billion in 2025 at a 32.6% CAGR.

Credit: Research and Markets

Banking-as-a-Service (BaaS) also enables non-bank entities to embed financial services such as wallets, savings, and credit. This BaaS segment is expected to grow to USD 74.8 billion by 2030.

In addition, cloud-native banking cores allow digital lenders and microfinance institutions to launch services cost-effectively and scale rapidly. For example, Google-backed Moniepoint uses Google Cloud solutions to enable small retailers across Africa to offer payments and banking services in remote areas.

Mobile applications serve as the primary interface for financial access. Through simple interfaces, businesses store money, send remittances, apply for microloans, and pay bills without needing traditional bank branches.

Alternative data models also allow fintechs to build credit scores for thin-file borrowers by analyzing mobile usage and payment patterns. Tala uses Android device data and behavioral data to underwrite loans while reaching millions previously excluded from credit.

Finally, distributed ledger technology (DLT) supports fast, low-cost cross-border payments. A noteworthy example is that of Everex, which has a blockchain-based corridor between Thailand and Myanmar. It allows migrant workers to send remittances in under a minute, which dramatically reduces transfer costs for vulnerable users.

Swich facilitates Digital Payment Gateway Platform

Pakistani startup Swich provides a unified digital payment platform that advances inclusive finance by delivering secure, accessible, and diverse transaction solutions.

The startup integrates an online payment gateway that enables businesses to accept payments through debit and credit cards, e-wallets, direct debit, and 1-Bill from a single interface.

Moreover, it offers Payment Links, a proprietary tool that allows merchants to generate and share payment requests instantly via platforms like WhatsApp or email. This solution eliminates the need for technical integration and streamlines the payment collection process.

In parallel, its Corporate Pay Out service streamlines global bulk payments to employees, suppliers, and partners.

The startup also introduces Bill-Out, a centralized bill management solution that connects businesses to a wide network of billers. It supports mobile top-ups and subscription payments through a single, integrated dashboard.

Additionally, Swich allows retail agents to earn commissions on digital services such as airtime, fund transfers, and bill payments.

ZAOSHINANI builds a FinTech Platform for Agricultural Cooperatives and Farmers

Kenyan startup ZAOSHINANI employs a digital fintech platform that expands inclusive finance. It connects smallholder farmers and cooperatives to real-time agricultural data and tailored financial services.

The startup operates through Zaoletu, which is a proprietary system that digitizes the entire agricultural value chain, from record-keeping and inventory tracking to payroll management and credit access.

This system enables cooperatives to automate member records, manage deductions, and deliver transparent updates via SMS. Farmers receive instant production data, access to historical performance, and fair credit based on output history.

Credit: ZAOSHINANI

Additionally, ZAOSHINANI integrates real-time analytics to support data-driven decisions, reduce manual processes, and improve operational efficiency across farming operations.

The startup further ensures accessibility through a user-friendly mobile app designed for varying levels of digital literacy.

6. WealthTech: AI-powered Solutions Saving 10-15 Hours Per Week

Digital-first client expectations, tokenized investment models, and rising demand for personalized, compliant services are positioning wealth tech as a core pillar of fintech.

Credit: The Business Research Company

Analysts project the wealth tech segment’s revenue will grow from USD 6.24 billion in 2025 to USD 10.82 billion in 2029 at a CAGR of 15.1%. This expansion is driven by platforms that combine personalization, transparency, and on-demand financial access.

GenAI copilots are redefining wealth advisory workflows. For example, Morgan Stanley’s wealth management division uses GenAI to enable advisors to auto-draft notes and proposals. This innovation is saving the organization 10-15 hours per week.

Tokenized funds and fractional shares democratize access to previously exclusive real-world assets. It opens private-market strategies to a broader investor base.

Robo-advisory platforms exemplify fintech’s ability to scale wealth access. For example, Wealthfront manages USD 85 billion by offering algorithmically personalized portfolios and lowering entry barriers for digital-native investors.

Similarly, consolidated dashboards, for example, eMoney, unify accounts, goals, and financial documents to enhance client visibility and control.

Blockchain-backed audit trails further improve compliance and risk management through real-time, tamper-proof records. This strengthens trust between investors, advisors, and regulators while safeguarding data integrity.

Cloud-native automation highlights many of these fintech solutions by enabling rapid development and deployment of wealth management tools. This involves robo-advisory engines that customize dashboards and offer secure services across diverse advisory offerings.

Big data pipelines and lakehouse architectures, paired with open-finance APIs, aggregate client holdings across banks, brokerages, and pensions.

Further, NLP chatbots guide businesses through complex decisions with personalized recommendations. AI-powered robo-advisory engines continuously optimize portfolios based on real-time market trends and user behavior.

Wealt offers a Wealth Management Platform

UK-based startup Wealt builds a digital wealth management platform that allows investors to consolidate, monitor, and grow their assets through a single, secure interface.

The platform lets businesses register various asset classes, track portfolio performance, and access curated investment opportunities typically reserved for high-net-worth individuals.

Moreover, the platform presents real-time visibility and equips businesses with intuitive tools that simplify complex financial data for informed decision-making.

Additionally, Wealt increases transparency and user experience by offering a smooth interface for daily wealth management.

The startup centralizes wealth oversight and expands access to exclusive deals. This allows a wider range of investors to take control of their financial future with clarity and precision.

UPTIQ enhances AI-powered Agents for Wealth Management

US-based startup UPTIQ builds an AI-driven platform that automates wealth management workflows using autonomous agents tailored for financial institutions.

The platform replaces manual processes and siloed systems with agentic apps that handle client onboarding, credit analysis, insurance review, and loan placement with speed and accuracy.

Credit: UPTIQ

Moreover, the platform extracts insights from documents and processes client data to support faster, more accurate decisions. It also streamlines workflows across compliance, risk, and operations while integrating with existing infrastructure.

Additionally, UPTIQ provides the AI Workbench, a no-code environment that lets institutions scale and customize AI workflows as their business evolves.

7. Open Banking: Market Expected to Reach USD 135.17 B by 2030

Regulatory mandates, consumer demand for personalization, and instant-payment innovation are actively driving the global shift towards open banking. For example, the EU’s Payment Services Directive (PSD2) and the US Consumer Financial Protection Bureau (CFPB)’s Section 1033 rule compel banks to share consumer data securely. This gives fintechs access to permissioned bank feeds and account insights.

Credit: Grand View Research

Presently, the open banking market is projected to grow up to USD 135.17 billion by 2030, reflecting a 27.6% CAGR. In the UK alone, 13% of digitally active consumers and 18% of small firms adopted open banking by early 2024. Moreover, Brazil’s open finance rails process 1.5 billion API calls weekly from 42 million consents.

Fintechs and banks are applying open banking across payments, credit, and onboarding. Revolut uses APIs to enable instant wallet top-ups and cross-border remittances. Lenders like Experian and FICO have permissioned cash-flow data into underwriting. This improves credit approvals for invisible borrowers.

Additionally, cloud-native payment infrastructure powers scalable settlement networks. For instance, FedNow handled 1.3 million instant U.S. payments in Q1 2025. API management platforms, for example, TrueLayer, offer secure, low-latency data connectivity.

Likewise, data aggregation services from Plaid allow over 8000 digital finance apps to turn raw bank transactions into actionable insights. Its USD 575 million secondary sale in April 2025 at a USD 6.1 billion valuation signals strong investor confidence in open banking infrastructure.

Behavioral biometrics tools from Alkami, for instance, use keystroke dynamics and screen interactions to detect fraudulent behavior in real time. In open banking, these tools add a critical security layer by verifying user authenticity during API-driven transactions and consent-based data sharing.

Cash-flow analytics engines like Experian’s cash-flow attributes and FICO’s upcoming score suite integrate open banking feeds to assess risk for buy now, pay later (BNPL) and thin-file borrowers.

Further, account aggregator frameworks enable fintechs to securely access consolidated bank data through user consent. As a core component of open banking, the frameworks facilitate real-time, permissioned data sharing for fintechs to deliver personalized financial products, credit scoring, and advisory services to underserved populations better.

YAXI applies Confidential Computing Technology for Secure Financial Workflows

German startup YAXI deploys an open banking platform that gives businesses direct access to user-authorized banking data. The platform does not expose users to third-party branding, terms, or privacy policies.

It uses confidential computing technology to protect user privacy and ensures that services request only specific, relevant data. This involves account holder name or balance thresholds while keeping all other information private.

Additionally, YAXI maintains optimal bank connectivity by actively multiplexing between PSD2, FinTS, and screen scraping, unlike traditional providers, limited to PSD2 APIs.

The startup also simplifies integration by providing software development kits (SDKs) that run across all major platforms and programming environments. These SDKs handle encryption and compliance processes automatically in the background.

Exthand builds Open Banking Data & Payment Stack

Belgian startup Exthand creates an open banking infrastructure that enables businesses to accept fast, secure account-to-account (A2A) payments without intermediaries.

The startup operates a suite of products, including EverLine, which integrates instant payments into checkout flows.

SkyBridge also gives unlicensed companies access to open banking data and payments. Moreover, EverShield lets regulated firms run secure open banking services within their cloud environments.

Credit: Exthand

The open banking infrastructure connects banks and supports variable recurring payments (VRPs), bulk payments, and customizable white-label and on-premise solutions.

Exthand owns its infrastructure, eliminates third-party fees, completes transactions in under ten seconds, and reduces breach risk by minimizing data exposure.

It also delivers premium API integrations tailored to specific business needs.

8. Regulatory Technology (RegTech): Singapore’s Monetary Authority Allocated SGD 100 M to Advance RegTech Solutions

Intensifying regulatory scrutiny, record-level enforcement fines, and the rising cases of financial crimes are driving regulatory technology within the fintech sector. Regulators are introducing stringent frameworks such as the EU’s Digital Operational Resilience Act (DORA) and the UK’s critical third-party regime. These rules demand continuous cyber-resilience proof and place cloud providers and analytics vendors like AWS directly under regulatory oversight.

Credit: Markets & Markets

Market forecasts highlight RegTech’s importance, estimating the global market to grow up to USD 19.5 billion by 2026 at a CAGR of 20.8%. Some project that the RegTech market will reach USD 155.5 billion by 2035 at a CAGR of 20.62%.

Credit: Roots Analysis

Financial institutions are prioritizing anti-money laundering (AML), counter-terrorist financing (CFT), know-your-customer (KYC), and customer due diligence (CDD) processes.

AI-powered tools, for example, ComplyAdvantage’s transaction-monitoring engine, reduce false positives by up to 70%. It reduces manual review workloads and escalates suspicious activities instantly.

Moreover, RPA handles repetitive compliance checks and reconciliations. Open APIs also integrate RegTech tools with core banking platforms and offer smooth data flows.

Fintech solutions use NLP to digest thousands of rulebooks daily and enable real-time updates. They also deploy DLT to create immutable audit trails that secure evidence and track compliance history.

National initiatives also back adoption; for example, Singapore’s Monetary Authority allocated SGD 100 million (USD 75 million) to advance AI and quantum-infused RegTech solutions.

Further, Italy’s Mopso raises EUR 1 million for AML tools, while India’s Data Sutram secures USD 9 million to expand its fraud analytics capabilities. Both these startups enable how RegTech strengthens compliance infrastructure within fintech by automating risk detection and regulatory reporting.

smarbl provides an AI-powered and Cloud-ready Financial Data Platform

UAE-based startup smarbl simplifies compliance management for financial institutions through its AI-powered solution SmartReg.

The SmartReg platform structures regulatory data using a pre-configured, open-source framework and generates reports. It also manages version control, tracks data lineage, and monitors submissions from a unified interface.

Moreover, the platform separates regulatory reporting from source systems through a data model and supports real-time monitoring with built-in validations, dashboards, and audit trails.

Credit: smarbl

smarbl enables businesses to extract data, adjust workflows, and deploy complex reports without information technology (IT) dependency.

Further, the startup uses SPARK, an open-source distributed computing system, and Kubernetes, a container orchestration platform, to scale its platform and optimize hardware performance.

RuleUp delivers a Regulatory Lifecycle Management (RLM) Platform

UK-based startup RuleUp offers an AI-powered regulatory technology platform that allows financial institutions to manage complex compliance requirements across global standards.

It delivers RuleUp RLM (regulatory lifecycle management), which tracks evolving regulations, detects compliance gaps, and provides actionable insights through an integrated dashboard.

The platform enables financial institutions to monitor risks in real-time, automate audits, and streamline regulatory workflows.

The startup also sends instant alerts, issues industry-specific notifications, and centralizes compliance timelines through a regulatory tracking system.

Additionally, it automates documentation processes and prioritizes risk to simplify regulatory adherence across banking, insurance, and fintech operations.

9. Embedded Finance: 96% of European Business to Roll It Out This Year

Consumer demand for smooth financial experiences, API maturity, and regulatory clarity is driving embedded finance across the fintech landscape. According to Solaris, 96% of European businesses plan to roll out embedded payments by 2025. This shift is due to the rise of plug-and-play BaaS platforms. For example, Stripe Treasury powers FDIC-insured Shopify Balance accounts and allows non-banks to offer full financial features within days.

Credit: Precedence Research

Moreover, the embedded finance market is projected to grow from USD 148.38 billion in 2025 to approximately USD 1.73 trillion by 2034 at a CAGR of over 31%. This reflects the expansion of embedded lending, payments, and insurance across digital ecosystems.

Visa Direct, for instance, enables instant driver payouts for Uber. Apple Pay also integrates Affirm’s BNPL feature into iOS. Also, Amazon embeds NEXT Insurance coverage during merchant onboarding.

RESTful application programming interfaces (APIs) connect fintechs and non-financial platforms to bank-grade infrastructure. These APIs embed payments, lending, or insurance into third-party apps. They also enable smooth fintech access without leaving the host platform.

Credit: Research and Markets

Additionally, identity and access management (IAM) tools verify businesses and screen for fraud at sign-up, while embedded widgets simplify transactions within apps. For instance, the global BNPL market is expected to grow by 13.7% on an annual basis to reach USD 560.1 billion in 2025.

Blockchain also contributes by facilitating fast and secure settlements. Fiserv’s FIUSD stablecoin pilot, for example, streamlines cross-border transfers through embedded channels.

Regulatory shifts from Europe’s PSD3 increase API openness and data protections, which make embedded finance more trustworthy and scalable.

Further, Solaris raised EUR 140 million to expand its BaaS offerings, while Alloy launched its embedded finance risk suite to attract banks and fintechs seeking compliance automation.

Elevate Money provides a Unified API-based Embedded Finance Platform

Australian startup Elevate Money enables digital businesses to integrate financial products directly into their user experience through a unified API.

The platform connects HR systems, accounting software, fintech platforms, and marketplaces with financial services. These services involve superannuation, life insurance, personal loans, and savings tools. HR systems also offer contextually relevant products at key customer touchpoints.

Moreover, the platform standardizes and simplifies integration by providing developer-friendly APIs, pre-approved content, and pre-integrated product options.

Additionally, Elevate Money ensures compliance and security through baked-in regulatory frameworks while streamlining onboarding and deployment across partner ecosystems.

The startup further turns financial services into an extension of digital platforms. It allows businesses to unlock new revenue streams, increase customer engagement, and improve financial outcomes for businesses.

Embifi enables an EV Financing, Lending, and Payments Platform

Indian startup Embifi provides an embedded finance platform that facilitates secured vehicle loans through non-banking financial companies (NBFCs) and banks.

The platform integrates loan application, KYC verification, underwriting, processing, and collections into a single system that digital platforms embed directly into their user experience.

Moreover, it offers loan amounts ranging from INR 50K to INR 400K with interest rates between 15% and 18%, and repayment tenures from 9 to 36 months.

Embifi also designs its financial products specifically for the electric vehicle (EV) sector to support sustainable transportation through structured lending solutions.

10. Central Bank Digital Currency (CBDC): 134+ Countries Trying Out CBDCs in 2025

Rising geopolitical pressure, competition from private stablecoins, and the demand for more secure payments are increasing the adoption of CBDCs globally. By 2025, 134 jurisdictions representing 98% of global GDP are actively exploring, piloting, or launching CBDCs.

Market analysts project that the CBDC market will expand to approximately USD 3 billion by 2035, growing at a CAGR of 19.2%. This surge reflects increasing commercial interest in sovereign digital cash. For instance, India’s e-rupee processes over 1 million retail transactions daily and enables programmable subsidy disbursements. This enhances the precision of monetary policy.

Likewise, China’s e-CNY is handling more than CNY 7 trillion in cumulative transactions that showcase its capacity for high-speed, high-volume retail payments.

Government disbursement use cases are also gaining traction. For example, Jamaica’s JAM-DEX reaches JMD 258 million in circulation across 282K wallets. Meanwhile, Hong Kong settled a HKD 6 billion multi-currency green bond natively using wholesale CBDCs via HSBC’s Orion platform.

Moreover, hybrid CBDC models that combine token-based and account-based designs offer the benefits of cash-like anonymity for users. These models also enable central banks to maintain account-level traceability for regulatory oversight. Smart contract layers add critical programmability and allow governments to automate conditional disbursements. This involves tax credits, targeted subsidies, or social welfare payments directly through digital currencies.

To ensure the usability of CBDCs in regions with low internet connectivity, central banks are integrating unstructured supplementary service data (USSD) technology into CBDC wallet designs. This integration, as demonstrated by Nigeria’s eNaira, allows businesses to conduct CBDC transactions securely without requiring internet access.

DLT serves as the backbone for many CBDC implementations because it provides tamper-proof, transparent transaction records. It also ensures that both retail and wholesale CBDC payments remain secure and auditable.

In addition, digital identity verification systems such as biometric authentication and electronic know your customer (eKYC) are crucial for CBDC ecosystems. They prevent fraud, support secure user onboarding, and enable regulatory-compliant access to CBDC wallets while maintaining user privacy where required.

Further, offline transaction capabilities, powered by near-field communication (NFC) or secure hardware wallets, are integrated into CBDC solutions. These modules ensure that CBDCs remain usable for consumers and merchants even in environments without continuous connectivity. This preserves the cash-like resilience that is a key design goal of digital sovereign currencies.

Intrasettle expedites Multilateral CBDC Cross-border Settlement Infrastructure

UK-based startup Intrasettle employs a blockchain-powered platform to support real-time, secure, and low-cost cross-border payments. It enables financial institutions to settle transactions using central bank digital currencies (CBDCs).

The platform connects central and commercial banks on a unified infrastructure. Central banks issue digital currencies, and banks use them to make peer-to-peer payments across multiple currencies without intermediaries.

Additionally, the platform uses tokenized cash backed by central bank money to carry out atomic settlement of transactions. This offers instant delivery and finality for both payments and tokenized securities.

Intrasettle applies payment vs. payment (PvP), delivery vs. payment (DvP), and token vs. token (TvT) models to reduce settlement risk and enable interoperability across financial services.

It also deploys a distributed architecture to eliminate single points of failure and enhance operational resilience.

Additionally, the multi-currency setup allows institutions to manage fragmented liquidity more efficiently.

Xaults yields Deep-tier Supply Chain Financing Platform

Indian startup Xaults develops a deep-tier supply chain financing platform. It offers programmable central bank digital currency (CBDC) solutions. This includes a merchant loyalty program, digital escrow services, and corporate expense management tools.

The financing platform uses programmable CBDCs to automate conditional payments, manage employee benefits, and provide real-time settlement, all through secure smart contracts.

The platform also enables banks to extend affordable credit to small and medium enterprises (SMEs) beyond Tier-1 by using distributed ledger technology (DLT) and smart contracts.

Moreover, the financing platform ties risk to the anchor by linking SME invoices to anchor invoices. It also automates loan disbursement, collections, reconciliation, and settlements through a fully digital process.

The platform also embeds compliance directly into each transaction by using smart contracts to enforce regulatory rules before processing any activity.

Further, Xaults protects its infrastructure with enterprise-grade blockchain and multi-layer cryptographic defenses. It also enables tailored governance through precise access and transaction controls.

Discover all FinTech Trends, Technologies & Startups

The future of fintech trends lies in next-gen technologies reshaping the global finance landscape. Quantum computing is improving transaction security and risk modeling, while edge computing is enabling real-time decisions at the device level.

5G and satellite internet are also expanding access to remote regions, and spatial computing is introducing immersive financial interfaces. Together, these innovations are redefining how financial institutions secure and deliver personalized services and are shifting the fintech industry over the coming decade.

The FinTech Industry Trends & Startups outlined in this report only scratch the surface of the trends that we identified during our data-driven innovation & startup scouting process. Identifying new opportunities & emerging technologies to implement into your business goes a long way in gaining a competitive advantage.

![Discover the Top 10 Compliance Trends & Innovations [2026]](https://www.startus-insights.com/wp-content/uploads/2025/09/Compliance-Trends-SharedImg-StartUs-Insights-noresize-420x236.webp)

{kind=link}